Suddenly has Arrived

Low interest rates pull expenditures forward and forestall bankruptcies, however, not forever. In “The Sun Also Rises” Hemingway wrote, “How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

Despite nine full years of zero-to-slight interest rates, “suddenly” has arrived. “Total US bankruptcy filings by consumers and businesses in March spiked 40% from February and rose 4% year-over-year to 81,590, the highest since March 2015,” writes Wolf Richter, “The Fed’s monetary policies have purposefully encouraged businesses and consumers to borrow. But debt doesn’t just go away. It accumulates. By now, an increasing number of businesses and consumers are suffocating under this debt overhang in an economy that never developed the ‘escape velocity’ needed – and hyped by Wall Street for years – to outgrow this debt.”

Payless Shoesource, headquartered in my old hometown of Topeka, Kansas, filed for Chapter 11 last week. The debt-saddled shoe vendor, valued its assets at between $500 million and $1 billion and its liabilities at between $1 billion and $10 billion and plans to immediately close nearly 400 of its 4,400 stores in an attempt to restructure.

Fortune reports, “Stores like The Sports Authority, American Apparel, Aéropostale, Wet Seal and PacSun are among the retailers to have filed for bankruptcy protection in the last two years, with some liquidating altogether. On Tuesday, Sears Holdings admitted there is 'substantial doubt' it can stay in business.”

Consumers are simply throwing in the towel with the retailers. Elliott Wave writes, “The latest analysis by the Consumer Federation of America finds that the number of Americans defaulting on their student loans jumped by 17% in 2016. By the end of last year, 4.2 million student loan holders were in default. The same goes for subprime auto loans. Fitch Ratings reports that the 60-day delinquency rate hit 9.1% in January, up from 7.9% a year earlier. Trends in used car prices, which tend to be a leading indicator of defaults, suggest that the problem will intensify.”

However, the Fed, figures its work is done. “The noisy verbiage in the Fed minutes with respect to the start of balance sheet shrinkage amounted to a declaration of ‘mission accomplished’, writes David Stockman. “But at least when George W. Bush landed on a US aircraft carrier to claim victory Baghdad was indeed a smoking ruin.”

The folks at ZeroHedge offer more bad news.

It's been more than seven years since the 'great recession' officially ended, but while Fed policies have successfully generated massive asset bubbles which have accrued solely to the benefit of America's wealthiest, the majority of American families remain as vulnerable to financial disaster as they were during the height of the crisis.

In fact, a recent study found that some 50% of Americans are woefully unprepared for a financial emergency with nearly 1 in 5 (19%) having absolutely no savings set aside to cover an unexpected expense. Meanwhile, nearly 1 in 3 (31%) Americans couldn't write a $500 check to cover an unexpected household emergency expense if they had to, according to a survey released by HomeServe USA, a home repair service.

Moreover, a separate survey released Monday by insurance company MetLife found that 49% of employees are “concerned, anxious or fearful about their current financial well-being” with less than 40% reporting that they're "in control" of their finances.

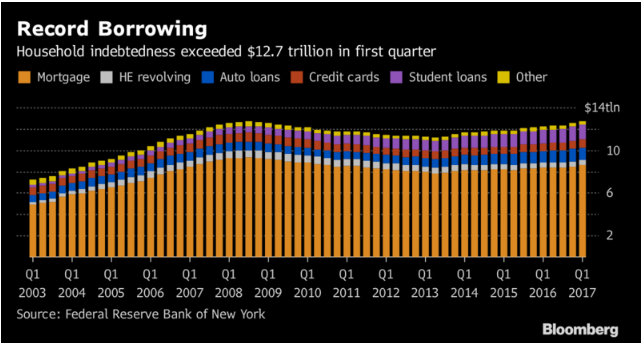

Meanwhile, Americans are closing in on carrying as much debt as when the economy hit the ditch in Q3 2008 while investors have ramped up a record amount of margin debt. “The amount investors borrowed against their brokerage accounts climbed to $528.2 billion in February, according to the most recent data available from the New York Stock Exchange, released Wednesday. That is up 2.9% from $513.3 billion in January, which had been the first margin debt record in nearly two years,” writes Ben Eisen for MarketWatch.

This is likely no spike, but a trend.