History Repeats: First Mortgages, Now Car Loans

When did The Wall Street Journal report the following?

The scope of false applications is hard to quantify. PointPredictive, which sells software to detect loan fraud, estimates that more than a fifth of _____ loans have inflated incomes. The company examined loans made over the past four years where lenders obtained borrowers’ personal records, and compared those with the income stated on applications. Its data can’t distinguish who is responsible.

In 2004 or 2005, the above blank would have been filled by “home.” On December 21, 2019, it was “auto” that filled the blank in Ben Eisen’s and AnnaMaria Andriotis’s piece in the WSJ, which highlighted Mirna López, with a $660 monthly income, buying a used 2018 Nissan Pathfinder with a car loan requiring a monthly payment of $809.

How could that be? An enterprising employee at the dealership filled in a $7,833 monthly income for Ms. López. And why not, as Eisen and Andriotis write,

Dealerships now make more money arranging financing than selling vehicles. If a car loan goes bad, it isn’t usually the dealership on the hook. When a borrower defaults, the lender can repossess the car and try to resell it. Often, though, that isn’t enough to cover the borrower’s unpaid balance, and the lender can write off the loss and can send the borrower to collections.

Product margins are skinny and technology has taken away the asymmetric knowledge advantage dealerships once had. So, once a customer falls in love with their new pride and joy, the hapless customer is sent to The Box. Adrienne Roberts wrote for the WSJ last year,

The high-pressure sales tactics often used in the finance office have long been a source of anxiety for consumers, analysts say. Privately, some dealers call the finance office “the box,” a reference to the holding cell to which movie star Paul Newman was sent in the 1967 movie “Cool Hand Luke.”

Grant’s Interest Rate Observer mentioned a recent WSJ article that “described how dealerships inflate borrowers’ income on loan applications and tell the customers to stop paying the auto loan tied to the trade-in vehicle--after they pass muster for a new one, of course. It’s hard to see how this is bullish for the institution of credit.”

Headline unemployment rates are very low. The president contends this economy is unbelievably strong. Yet, as Wolf Richter writes,

All combined, prime and subprime auto-loan delinquencies that are 90 days or more past due – “serious” delinquencies – in the fourth quarter 2019, surged by 15.5% from a year ago to a breath-taking historic high of $66 billion, according to data from the New York Fed released today:

If that’s not startling enough, Richter continues,

Seriously delinquent auto loans jumped to 4.94% of the $1.33 trillion in total loans and leases outstanding, above where the delinquency rate had been in Q3 2010 as the auto industry was collapsing, with GM and Chrysler already in bankruptcy, and with the worst unemployment crisis since the Great Depression approaching its peak. But this time, there is no unemployment crisis; these are the good times: (emphasis added)

Where do these ill advised auto loans go? To Wall Street of course. Richter explains,

Subprime auto loans are often packaged into asset-backed securities (ABS) and shuffled off to institutional investors, such as pension funds. These securities have tranches ranging from low-rated or not-rated tranches that take the first loss to double-A or triple-A rated tranches that are protected by the lower rated tranches and generally don’t take losses unless a major fiasco is happening. Yields vary: the riskiest tranches that take the first loss offer the highest yields and the highest risk; the highest-rated tranches offer the lowest yields.

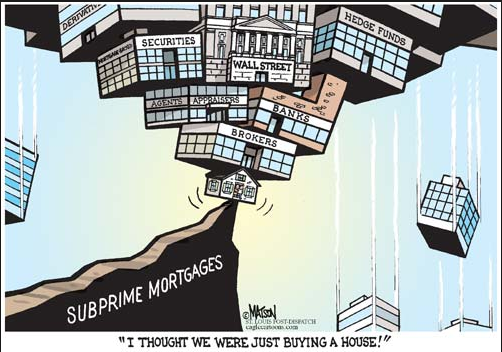

To fans of The Big Short, this should look and sound familiar. Dealerships and consumers have joined hands to jump into the canyon of bad incentives. As the old saying goes, “knowledge in finance is cyclical, not cumulative.”

Repo men and women, get ready.